It’s year-end tax planning time…

I’m sure you’ve heard of tax-loss harvesting—the process of selling investments in a taxable investment account at a loss to realize the loss and be able to offset future capital gains. Financial advisors and CPAs often recommend this strategy and robo-advisors will even take care of it for you. It’s a strategy worth exploring and if you’re not taking advantage of market declines you might be missing opportunities to save on future capital gains taxes.

From my CCO (chief compliance office) 😀: It’s important to understand there is more to tax-loss harvesting than just selling losers and reinvesting. You should be aware of the wash sale rule and other implications that could impact your personal situation. I highly recommend working with a professional when it comes to taxes.

Opportunity With Gains

There’s another type of tax harvesting that you may not have heard of, but it’s just as powerful as tax-loss harvesting. Allow me to introduce you to tax-loss harvesting’s polar opposite, tax-GAIN harvesting. Unlike tax-loss harvesting, due to an accelerating capital gains tax rate based on income, tax-gain harvesting isn’t a strategy that is available for everyone, which is probably why you have never heard anyone talk about it before.

Similar to loss harvesting, gain harvesting involves selling investments in a taxable account but instead of banking losses to offset gains, you realize long-term capital gains at a lower tax rate than expected in the future. That’s a mouthful I know, so let me share an example.

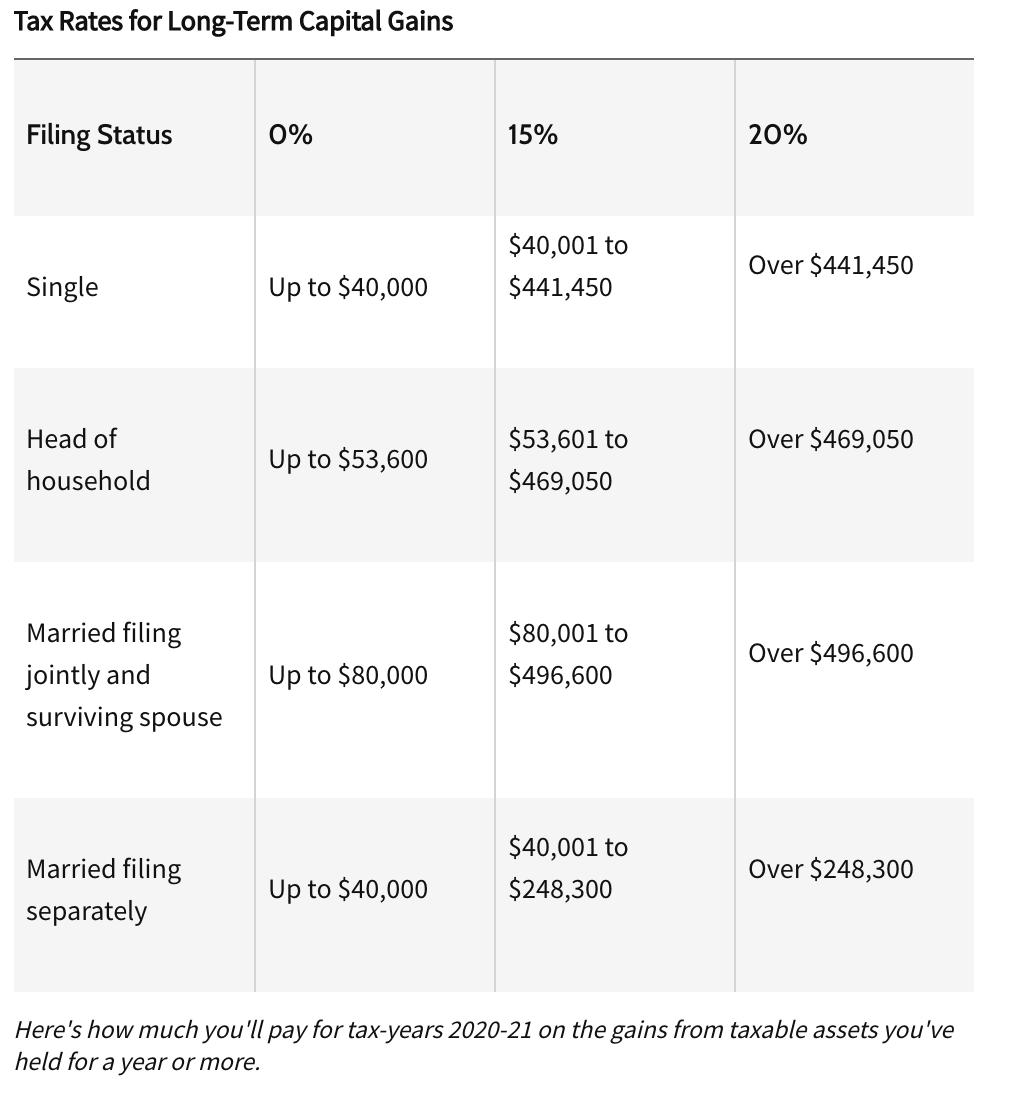

You’ve been fortunate to be able to save and invest over the last few years in a taxable investment account and have seen some nice gains in your portfolio. As you head into year-end you realize your income will not exceed $40,000 as an individual ($80,000 married filing jointly), which means any long-term capital gains realized will be taxed at 0%. In order to take advantage of the greatest tax rate ever, 0%, you sell some of your investments to book the gain and re-establish your position for the future.

Calculating how much you should sell to maximize the 0% capital gains rate should be something you work with a professional to make sure you get it right.

Still Works In 15% Capital Gains Bracket

Obviously, taking advantage of a 0% tax rate is something you should seriously evaluate, but tax gain harvesting can still be an effective strategy even if you find yourself in the 15% capital gains bracket.

The strategy can still be effective if you anticipate higher capital gains taxes in the future. Maybe you’ve had a reduction of income this year or you anticipate a bump in your income in the future, you may want to maximize the 15% capital gains taxes—pull some of those future 20% capital gains into the 15% bracket.

Deciding to harvest gains is a little more complicated than I laid out—there are a number of factors to consider if it makes sense, so I want to stress the importance of working with a CPA or financial advisor to make sure you don’t cause more harm than good. There can be negative implications on Social Security taxation and health insurance subsidies just to name a couple of potential mistakes.

It might be hard to pull the trigger and realize gains because of the emotional pain of paying taxes. But if you take a bigger picture look at your overall financial plan, your goal should be to try to smooth out your effective tax rate over time and accelerate capital gains taxes into lower tax rate years is a smart strategy (assuming it fits within your overall tax planning) to consider.

Definitely harvest your losses—get something out of down markets, but don’t neglect your gains.

Disclaimer: Nothing on this blog should be considered advice, or recommendations. If you have questions pertaining to your individual situation you should consult your financial advisor. For all of the disclaimers, please see my disclaimers page.

1 thought on “Harvesting Gains”

Comments are closed.