“Diversification means always having to say you’re sorry.”

-Michael Kitces (I’m not sure of the origin, but I heard it from Michael, so he get’s the credit)

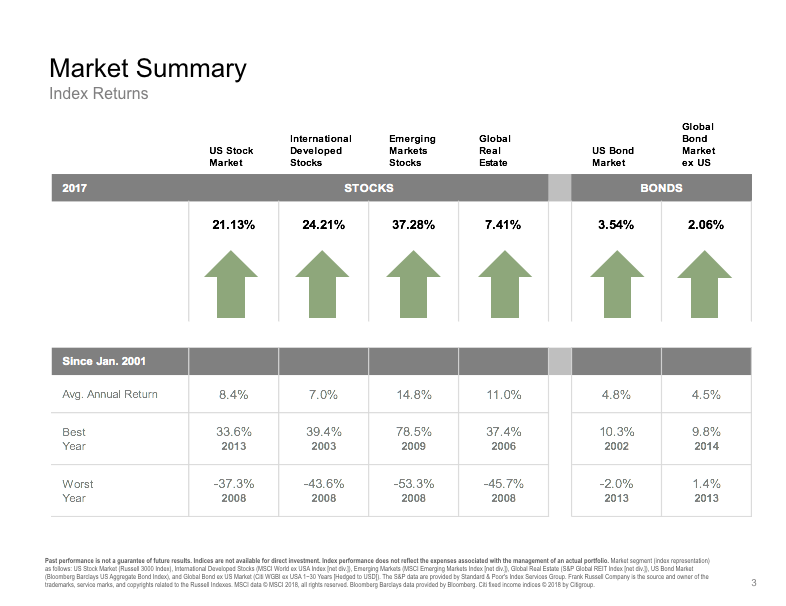

Financial advisors who have had to apologize for keeping their clients disciplined and in a globally diversified portfolio can breathe a little easier after 2017. It was in 2017 the international markets finally decided to join the party, and it became the year of no apologies for diversification.

Look at that chart…beautiful green arrows all around and international markets leading the global growth story. For nearly six years, financial advisors had to explain and, as Michael Kitces describes it, apologize to their clients for continuing to hold international funds in their clients’ portfolios.

Source: YCharts

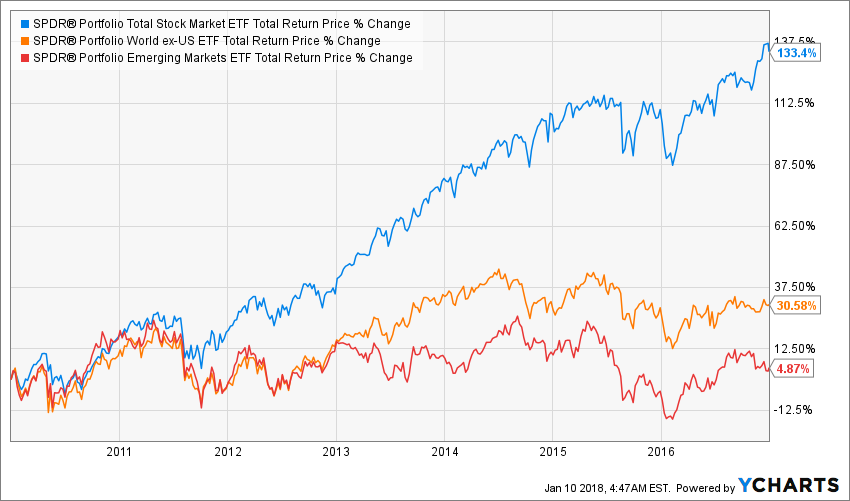

U-S-A, U-S-A, U-S-A…

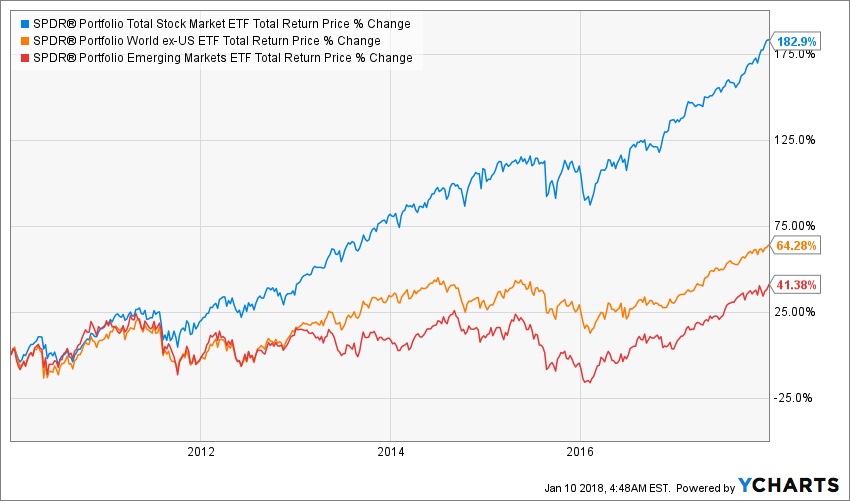

From 2010 through 2016, US investors suffering from home country bias were rewarded, while disciplined investors holding a globally diversified portfolio were annoyed (maybe even a little disappointed). Just look at the outperformance. Despite overwhelming evidence supporting a globally diversified portfolio, many investors lack the proper diversification and are significantly overweight the United States (I’m referring to US investors, but as I’ve discussed before, investors in most countries exhibit the same behavior). And as you can see, those investors have done quite well in recent years, but my fear is overconfidence of getting it “right” will prevent these investors from re-evaluating their allocations and adding the international exposure they need until it is too late. I’m not suggesting the US markets won’t continue the strength we’ve seen recently, but investors with home country bias have dodged a bullet in that their bias has worked in their favor–that won’t always be the case.

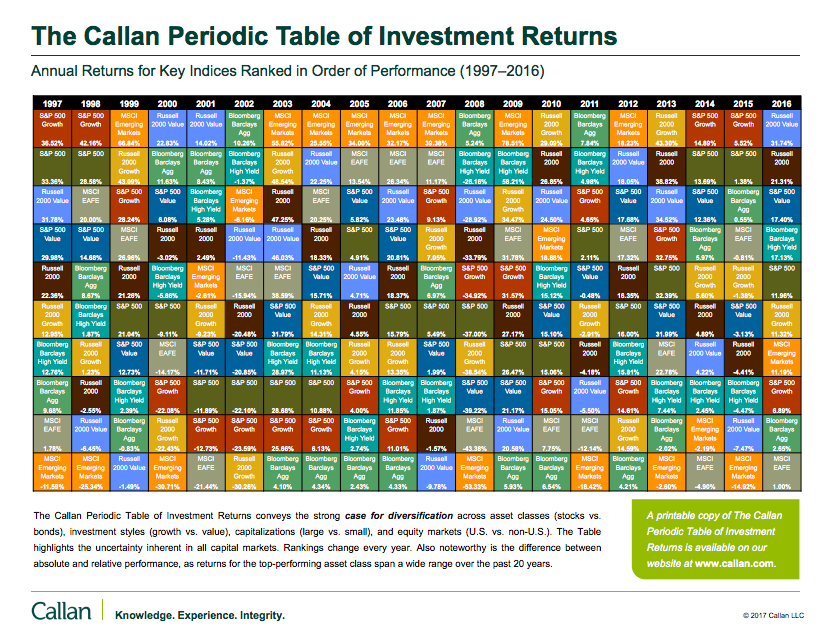

Most investors should be familiar with this chart, the Callan Periodic Table of Investment Returns. For those seeing it for the first time, this important table is all the evidence you should need to hold a globally diversified portfolio. As you can see, there is absolutely no rhyme or reason to the movement of the colors, which represent different areas of the market. What’s on top one year is on the bottom another. Just pick a color and follow it through the chart–it’s a rollercoaster. But, by holding a diversified portfolio of all of the colors, investors end up smoothing out the ride and also eliminating the need for trying to guess which color will be on top from year to year. Note: Yes, some investors are able to dedicate the time to be more active in their strategies and overweight their portfolios based on trend following, which can lead to benefiting from overweighting the best performers and underweighting the worst. BUT, for most investors, that is not a realistic option and it’s extremely hard to do successfully over the long term.

Proactive vs. Reactive

My dad always told me it’s best to look for a new job when you already have one–don’t wait until you NEED a new job. If US heavy investors have been playing with fire and have yet to get burned by not having the proper international exposure, it might make sense to revisit their financial plan, revisit their goals and revisit their investment strategy before needing some bacitracin. There will come a time where a lack of diversification will become a hindrance, and why not make an adjustment before it’s too late?

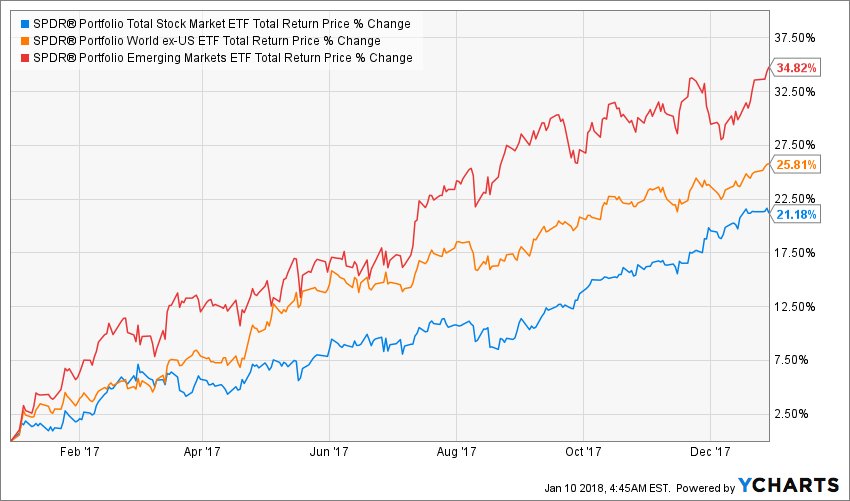

2017, if anything, should have at least opened the eyes of the investors with home country biases; not because the US market did poorly because it actually did great. But, because international markets, both developed countries and emerging markets, did even better. Disclaimer: I am not recommending an allocation change to chase the performance out of the international markets. That is the wrong reason for moving to a globally diversified portfolio. I’m arguing investors should have always been holding a globally diversified portfolio, and if they are not, let 2017 remind them that the US is not always number one.

Source: YCharts

It would not be unreasonable to expect to see at some point a reverse of the trend from the last 6 years, and if/when this occurs investors with a globally diversified portfolio will be rewarded for their discipline and investors with home country biased will be disappointed. Investors believing in value investing and reversion to the mean might see opportunity in the chart below, which I’ve updated to include 2017. Even with last year’s performance in the international markets, there is still a pretty big gap between US and international markets…

Source: YCharts.com

Closing Of The Gap

There are a few ways for the gap to narrow:

- US markets decline

- International markets continue on a tear

- US markets growth slows but doesn’t necessarily decline and international markets continue to grow

- Etc.

Which one will it be? How fast will it occur? Will it occur? No one has the answers, despite how convincing they might be, which is a strong argument for holding a globally diversified portfolio is a good fit for most investors.

Take this as one more reminder to check your portfolio, consult your financial advisor and determine if any adjustments to your portfolio are needed.

Additional Reading:

AAYB: Home Country Bias and Your Portfolio

AAYB: Home Country Bias Check-Up

No more….

Disclaimer: Nothing on this blog should be considered advice, or recommendations. If you have questions pertaining your individual situation you should consult your financial advisor. For all of the disclaimers, please see my disclaimer page.

1 thought on “No More Apologies For Global Diversification”

Comments are closed.